Sharing Economy in the Telecommunications Industry: Open Access in Fibre Networks – Part 2

Open Access Networks (OAN) help telcos leverage the power of the sharing economy and accelerate progress through a collaborative approach. As OANs are increasingly adopted for mobile communication under the MVNO/E/A model, Mukesh Binani examines the model implemented in Fibre Networks.

Let’s face it – every service provider wants to deliver their services via fibre networks to gain the benefits of high speed connectivity (or some say next generation connectivity) for overall customer satisfaction. But installing fibre networks is costly and not an investment every service provider can make. However, one of the fastest ways to deliver the benefits of fibre networks to customers and businesses while overcoming its limitations is through the Open Access Networks (OAN) model, which enables multiple stakeholders to provide services through one shared network.

The main principle behind OAN is to provide access on equal terms which results in fair and transparent service for service providers and greater choice for consumers. It is also more sustainable to connect to existing networks instead of building from scratch. Needless to say, it results in a lower cost of services and benefits all stakeholders involved.

Key Players

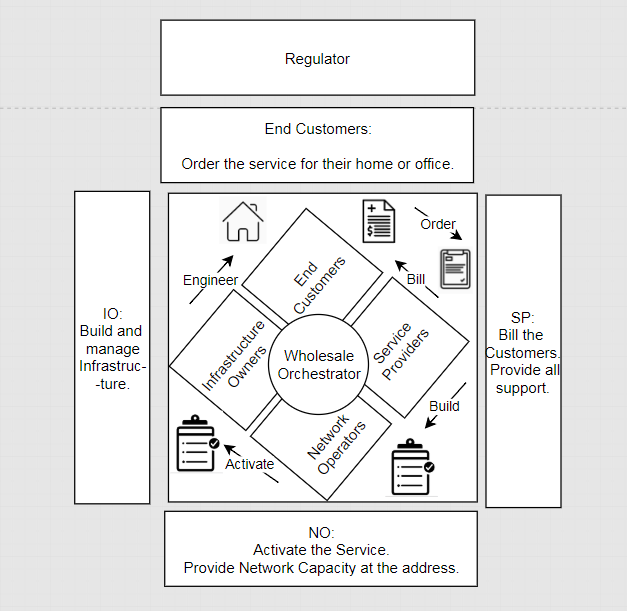

There are five key stakeholders in the open access model:

- Service Provider (SP) - The retail provider who pays the wholesale access provider for operations. They do the marketing and sales and provide services to the end customers.

- Network Operator (NO) - The provider (and maintainer) of active network equipment (routers, switches, transponders, etc). It could be any telecom operator or municipality providing neutral networks.

- Infrastructure Owner (IO) - The provider (and maintainer) of passive infrastructure (trenching, cable duct laying, etc). It could be utility, housing and transport companies or even municipalities.

- Wholesale Access or Platform Provider - To orchestrate all the above entities and aggregate the offerings* to efficiently provide services.

- End Customers - Users who can choose between different services from any service provider seamlessly. For the end customer, the service provider (SP) is the point of contact for bills, services and all technical issues. It can be both residential or business customers.

*There can be some content providers or OTT players also providing services under the wholesale access approach. In some scenarios, wholesale players can help to further reduce the cost for other entities by providing other white label services like billing and fault management systems, servers and operational support.

The Open Access Ecosystem

Sometimes Service Providers and End Customers are called northbound or upstream entities, while Infrastructure Owners and Network Operators are referred to as southbound or downstream entities in the wholesale platform model. These entities can be different players, or a single entity can play multiple roles.

The wholesale partnership model can be represented as follows:

Role of the regulators

One key player not mentioned in the arrangement above is the regulatory body. These governing bodies define the rules for open, independent, transparent and non-discriminatory participation in OAN.

The main role of regulators is to:

- Enable fair competition

- Establish rules for companies playing multiple roles to ensure fairness for all stakeholders involved

- Make pricing transparent

- Ensure fair access

- Quality of Service (QoS) for all

- Oversee mergers and ensure compliance to the regulatory framework

- Establish network coverage even in remote areas

- Foster a flexible regulatory environment to attract new investment

- Reduce monopolisation by incumbent operators

By providing open government policies and financial incentives, regulators maintain the balance of investment and sharing access.

Benefits for stakeholders

The main goal of the open access approach is to ensure:

- End customers can choose their service providers from the marketplace freely, with a single bill and single point of contact irrespective of the underlying networks used to provide the services.

- Service providers can reach as many end customers as possible without being limited by ownership of real network assets.

- Lower barriers to entry for new service providers, resulting in a faster time to market and increased competition.

- IO/NO utilise their network assets to the fullest, generating greater returns on their investment.

- Wholesale providers offer a secure and independent platform with open APIs for all the key stakeholders involved.

Overall, the idea is to generate a low-risk investment model for all entities.

Why does the Open Access approach make sense?

- Fibre is becoming the infrastructure of choice worldwide, and a lot of countries across the globe are adopting the open access model to fast track its implementation. It is already a proven model in Sweden and Norway where internet connection speeds are among the highest in the world. Its usage is also growing in other countries such as the UK and US.

- It also enables use of fibre owned by government bodies such as municipalities. Recently, there was a report that San Francisco is building its own $1.9 billion Open Access Fibre Network.

- This enables the provision of network coverage to areas where private or incumbent players may not be keen to invest. Lots of OECD countries are developing Public Private Partnership models to launch fibre networks.

In the final part of the blog series, we will look at the technical architecture, key features, revenue models and implementation of Open Access Networks.

Read part one of this series on the sharing economy here